TWO HUNDRED PERCENT RETURN IN LESS THAN A YEAR, WITH LESSONS TO BE LEARNED!

Luby’s, Inc. (LUB) – The Long and Winding Road

Ever since Chris and Harris Pappas became involved in Luby’s in 2001, investors have hoped for either a turnaround in the operations of the company, the sale of the buildings and land that the company owned, a merger with their restaurant company or a combination of these. After almost 20 years, on June 3rd of 2020, Luby’s announced it would finally pursue the sale of all its operations and assets and distribute the net proceeds to stockholders. The final distribution payment is expected to be paid in June of this year.

The following is a summary of the series of events that led to liquidation of the public company and the lessons to be learned.

Back in the Day

Luby’s, Inc. (LUB) has been publicly held for almost 40 years. Some of us remember when Luby’s traded as “best of breed”, writing the book in terms of operating culture within the cafeteria segment of the restaurant industry. Profitability became less consistent at the end of the 1990s but the company was still paying an $0.80 per share dividend as late as 1999. By ’01, however, the company reported a $49M loss (including a $30M write-down). In the same year, Chris and Harris Pappas invested in Luby’s via a $10M convertible note that converted into 2M shares at a price of $5.00 per share (9% of the company). Chris Pappas was named President and CEO, while Harris Pappas was named COO of the company. The company at that time operated 219 Luby’s restaurants, under 125 of which the land and building were owned.

Time Flies When You are Having Fun

The Pappas brothers are highly respected Houston-based restauranteurs that operate a group of restaurants such as Pappadeaux Seafood Kitchens and Pappasito’s Cantinas. However, since taking over the company, Luby’s lost money in 12 of the 20 years the Pappas brothers have been in charge. In addition to the typical challenges of managing over 200 cafeterias, it didn’t help that the company also made two unsuccessful acquisitions. In 2010, the company acquired the Fuddruckers chain for $63M in cash, at which time Fuddruckers operated 59 restaurants (of which 22 owned land and building). There were also 129 franchised restaurants. On December 6, 2012, Luby’s acquired the Cheeseburger in Paradise chain for approximately $10.3 million in cash, at the time operating 23 full-service restaurants within 14 states.

As the table below shows, the Luby’s brand had been shrinking ever since the Pappas brothers took over. After four years of growth, the Fuddruckers brand also began to shrink. However, the company still owned the buildings and land under a significant number of Luby’s and Fuddruckers restaurants. The poor operating results were obscuring the value in the company’s real estate.

Large Shareholders Become Impatient

In November of 2018, 9.8% long term shareholder, Jeff Gramm, co-founder of Bandera Partners, initiated a proxy contest by nominating four potential board members including himself, his father (former Senator Phil Gramm) and two others. At the time the stock was trading for approximately $1.50 per share, down from a peak of $25. Since the Pappas brothers owned 36% of the stock by then, the proxy fight was doomed to fail from the start. However, after 20 years of waiting for management to turn the company around, some large shareholders, including Bandera and another 9% long term shareholder, Hodges Capital, were trying to unlock the value in the company’s real estate.

Comments from Gramm’s proxy letter to management:

“At the same time, I have a fiduciary responsibility to the investors in my fund, and I’m writing today to tell you that what’s happening at Luby’s is simply not working. The Fuddruckers and Luby’s restaurant concepts do not generate a sufficient return on capital to justify the investments management is making, under your direction and supervision, into the business. The strategy of plowing cash flows back into restaurants works with good concepts like Pappadeaux and Pappasito’s, but it has been a failure at Luby’s. Capital expenditures since fiscal 2008 have totaled $235 million dollars, about six times the company’s current market capitalization. The return on this investment has been dismal, and to pay down the debt you have accumulated in the process, Luby’s is liquidating the most valuable asset shareholders own, the company’s real estate.

“Luby’s owned real estate portfolio is tremendously valuable. Its appraised value (net of debt) is over $4.00 per share of Common Stock, as compared to its current stock price around $1.40. 1 It is brutally painful to watch the Company chisel away at its real estate portfolio to fund low-return investments into the business. Since fiscal 2008, Luby’s has sold $88 million of assets. This capital, more than double the current market capitalization, is gone and forever lost to shareholders. Given the futility of recent investments into Luby’s and Fuddruckers, has the Board considered a capital allocation strategy that preserves the real estate value and returns capital to the owners of the company, the shareholders?”

While the proxy contest failed, it did force management and the Board to take steps that led to the eventual liquidation of the company. What follows are a list of events that took place after the proxy contest, according to the Board proposal for liquidation.

In March of 2019, the company began analyzing cost reduction measures using an outside third party.

In May of 2019, the company began considering strategic alternatives including the sale of Fuddruckers operated restaurants and real estate assets.

In August 2019, the company adds two new independent directors.

In September 2019, the company creates a Special Committee to look into possibilities such as:

Continuing as an existing operation

Selling the company as a whole

Selling individual assets including the real estate in separate transactions, followed by the distribution of net proceeds to stockholders

Selling the restaurant operations while retaining the real estate and converting to a REIT

By December 2019 the company had contacted 15 investment banks, received 6 proposals, and selected Duff and Phelps to serve as financial advisor.

In January 2020, a deal to sell Fuddrucker’s falls through.

From February to May 2020 Covid-19 impacts operations, but sale process continues.

A Plan

On June 3 ’20, the company issued a press release saying they would pursue the sale of its operating divisions and assets, including real estate, intending to distribute the proceeds (net of debt and other obligations) to shareholders. Interestingly Duff & Phelps estimated the potential liquidation proceeds, net to stockholders from $127M to $172M or $4.15 to $5.62 per share. (Turning out to be a good estimate.) However, the press release issued on September 4, ’20, in the middle of the pandemic announcing the plan of liquidation, estimated the net proceeds to shareholders would be $92M to $123M or $3.00 to $4.00 per share, presumably due to the impact of Covid-19.

The Payoff

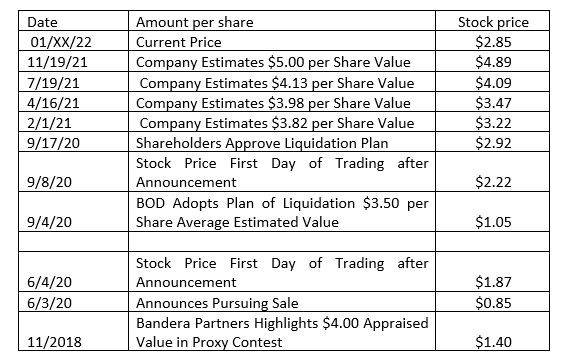

The table below shows the prices of the LUB common stock from 11/18 at the time of the proxy contest until the current time. It is clear that even if an investor waited until the liquidation plan was officially approved on September 17th, 2020, the returns were substantial. There was also ample time for an investor to acquire shares substantially below $2.00.

On November 17th, 2020, shareholders approved the liquidation plan. The stock closed at $2.92 per share on that day. Because the company owned land and buildings and operated two different concepts, including one with a significant franchisee base, the company chose to pursue the sale of each concept and the land separately to maximize the value to shareholders.

The first transaction occurred on March 17th, 2021 when the company sold 8 company owned stores (including the land) to Black Titan Holdings, a large Fuddruckers franchisee. This was followed by the sale on June 17th, 2021 of the Fuddruckers franchise business to Black Titan Holdings as well. This business had 92 locations and was sold for $18.5M. This was a hard earned result, since the company had contacted over 150 entities during the eight-month sales process.

Four days later the company announced an agreement to sell the Luby’s cafeteria business (32 locations) to Calvin Gin for $28.7M. It is important to note that the sale did not include the real estate that Luby’s owned under 25 of those locations. The company’s advisors had contacted over 235 entities while conducting the sale of Luby’s.

Finally on September 20th, 2021, the company announced that STORE Capital was acquiring 26 real estate properties for $88M. The company had sold nine properties in FY20 for $23.7M and an additional eleven properties in FY21 for $32.1M.

According to SEC filings, the increase in value from the $3.50 per share to $5.00 per share in total distributions was almost equally divided between the improving cash flows of the underlying stores and higher realizations of proceeds from the sale of the real estate. However, it is clear that the real estate was significantly more valuable than the store operations.

The Takeaways

(1) Shareholders without very long term patience did not benefit from the ultimate liquidation of the Luby assets. However, those that held on were able to recoup part of their investment. Later stage investors, along with Bandera and Hodge, that arguably instigated a change in management’s willingness to monetize the corporate assets, were able to make substantial profits.

(2) No matter how much of a discount there is between the public and private market value, there has to be a willingness of the controlling shareholders to realize it. Management controlled over 36% of the shares at the time of the proxy contest. Chris Pappas had been earning salaries of $400K-$500K for years and was receiving total compensation of between $700K-$1M before 2018. Harris Pappas also earned a $400K salary for years as COO.

(3) The Pappas brothers are both over the age of 70, which could have provided motivation to finally liquidate the company assets.

(4) Owning, rather than leasing, the land and the buildings can provide shareholders with non-operational value creation, if and when management is willing to monetize the underlying property. The lower current “cash on cash” operational return on investment is offset, especially during inflationary times by long term appreciation of the underlying real estate. A lower current cash breakeven point should also not be underestimated as a source of comfort.

Roger Lipton of Lipton Financial Services Contributed to this analysis.