$TLFA, Fun with Models

Low Number of Outstanding Shares Leads to Wide Disparity of Outcomes

Tandy Leather Factory is slowing getting current on their SEC filings in the hopes of getting relisted by the September 28th deadline to avoid their stock going dark. Most, if not all, brokerages are currently only allowing liquidation trades in the company’s stock. While the company may not make the deadline, we do believe the company will eventually become compliant and normal trading will resume in the stock.

Quick background. On August 14th, 2019 the company announced that it commenced an independent investigation into certain aspects of the Company’s methods of valuation and expensing of costs of inventory and related issues. Due to delinquencies in filing with the SEC related to the investigation and the necessary restatements, the company was declared delinquent in its filings by Nasdaq and was relegated to the “pink sheets” in August 2020. In June, 2021 the company began filing their delinquent filings and have filed all of the 2018 and 2020 10Qs and 10Ks. The company still needs to file 2021 10Qs to get current.

Using the restated financials, I have built an extremely simplistic earnings model in order to understand some of the earnings sensitivities to changes in revenue, gross margins and operating expenses. The company only has 8.5M shares outstanding, so small changes to the inputs produces an extremely wide range of outcomes. These are the types of scenarios I get excited about because the large uncertainty of outcomes typical causes investors to avoid companies like TLFA, creating a potential highly profitable investment opportunity.

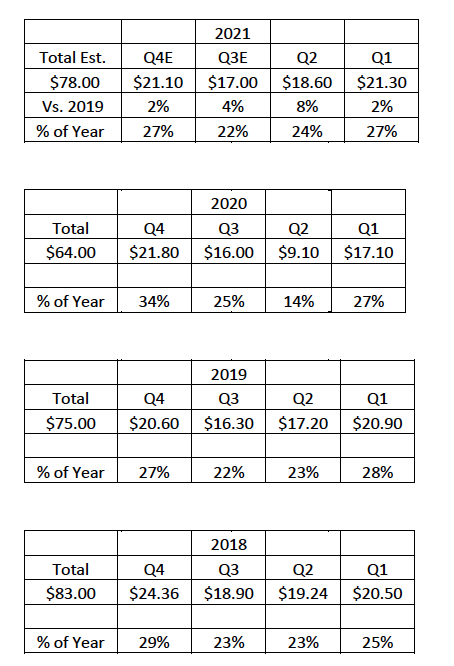

Let’s start with revenue:

Like most retailers, because of the large disruptions to store operating hours and store closures, it is difficult to get a true baseline run-rate of current sales. In spite of not issuing current 10Qs for 2021, the company has released quarterly sales figures for the first two quarters of 2021. So far, the sales have been trending 2-8% ABOVE 2019 levels. These sales are stronger than they first appear because the company is operating 11 fewer stores than 2019. Not surprisingly, Q1 and Q4 produce the strongest quarterly sales.

I hate “single point estimates” and refuse to calculate one in this post. In fact, the main purpose of this exercise is to get a feel for 2022, not 2021. As you can see from previous years, Q3 revenue typically dips from Q2 and Q4 is about 25% above Q3. For 2021, I looked at Q3 and Q4 compared to 2019 and didn’t want the numbers to be too far ahead of what happened in Q1 and Q2. $78M in sales looks “reasonable”, but I would not be surprised by $73-$80M either. Again the point is just to get something down on paper.

Next up, Gross Margins:

Now that TLFA has released audited, restated financials for the past several years, we have a better understanding of recent historical gross margins. Before 2019, the company generated gross margins around 60-61%. However, the last two years the gross margin has been only about 56%.

Looking at the disclosures in the last two 10Ks, it appears as though the days of 60%+ gross margins may be over. For 2021, given the commentary about inflation and shipping cost increases from most retailers, 56% gross margins may be tough to achieve in 2021. However, from a long-term perspective, I think a good starting point for gross margins could be 56-58% until there is more information.

Finally, Operating Expenses and Taxes:

In the lastest 10K, the company disclosed what it considered to be “adjusted” or more normalized operating expenses. While “normalized” can always be debated, we will go with TLFA numbers for now. For 2020 the company said $37.3M was the run rate. For now I will use $37M-$40M on a go forward basis. When the 2021 10Qs are filed, I will update the model. As far as the tax rate the company has stated it believes its long-term tax rate is 25-27%, so I will use 26%.

Putting it all Together:

Finally we get to the part where we try to answer the question, “What can TLFA earn on a “normalized” basis?” Considering we could get updated numbers in the next few weeks, this post may not age well, but here we go anyway.

Assumptions:

· Revenue

o $73M seems sufficiently conservative

This would be below 2019 revenue. Some pent-up demand wanes and new merchandising and pricing do not stimulate enough demand.

o $80M seems sufficiently aggressive

The company has 11 fewer stores than when it did $83M in revenue.

At some point the new management should be able to improve sales through new merchandising and pricing. Online sales have been very strong and could provide incremental sales.

· Gross Margins

o 56% seems modestly conservative

Given all the headwinds of rising commodity and shipping costs 56% gross margins might be a bit aggressive to 2021, but maybe not 2022.

The company is carrying extra inventory that it purchased earlier than normal to avoid some of the added shipping costs.

o 58% seems sufficiently aggressive

Commodity costs and shipping costs may stay elevated longer than anticipated.

New pricing policies may have permanently reduced gross margins to below 60% for the foreseeable future.

· Operating Costs & Taxes

o $40M seems sufficiently conservative

Many companies are operating leaner than ever before.

The company could add some expenses back if sales growth is higher than expected or bonuses or other compensation is increased in the new competitive environment.

o $37M seems sufficiently aggressive

Simply assumes that 2020 run-rate is sustainable.

Filing of Qs will help establish more realistic run-rate.

o Tax rate of 26%

Company estimates future tax rate of 25-27%

· Shares Outstanding

o 8.5M

9M shares outstanding as of December 2020.

Company acquired 500K shares in January 2021 at $3.35 per share

Models

Putting it all together, I get a range of earnings per share of $0.09 to $0.83 per share. OK, I am already hearing, to quote Maggie O’Hooligan in Caddyshack, “Well tanks for nuthin!” As I mentioned before, the objective of this exercise wasn’t to get to a single point estimate, ala Wall Street, but to put together various scenarios to get a feel for the range of profitability the company could achieve in a normalized environment. As the company releases more financial data and I have the opportunity to talk to management about their future plans, we will be able to narrow my estimates. This is based on my years of experience in evaluating small companies and the quality of the management team to execute on the opportunities that are ahead. This also provides a framework for discussion with other investors on where they think revenue, margins and expenses may come in. This is really the main reason I like to do these exercises. There are a lot of other aspects of the company that are interesting that I may cover in future posts (i.e the potential for value realization of the corporate headquarters, the new distribution center and the possibilities to improve sales and profitability, increased online sales).

Conclusion:

The ability to analyze a “normalized” TLFA business model has been hampered by a lack of restated financials, combined with the effects of the pandemic. The new management team has not really had the opportunity to enact their plans to improve and grow the company. I do like the management team and the Board of Directors has several strong members that can add value and insights. While it is easy to take the range of earnings outcomes I created and just average them to get to about $0.46 per share and say the stock is trading at only 9X 2022 EPS, it is probably not that simple. My sense is that the company could earn that amount of money next year, but what is more interesting to me is what it could earn in 5 years. Before new management arrived in 2018, the company had become stale and complacent. The huge inventory accounting problems and subsequent SEC fine of the previous CEO (2 1/2 years as CEO and 16 years as CFO) highlight the need for a change.

We are long the stock and look forward to reviewing the 2021 SEC filings and the resumption of the ability to buy the stock. Stay tuned.

Thank you for the update.