MamaMancinci's - The Adults Are Now In Charge

New CEO/CFO/Controller/others focus on the three C’s strategy: cost, controls, and culture showing immediate results.

Attention To Detail Shows Immediate Results

Gross Margin improved from 11.8% to 24.7% Q/Q

Gross Profit dollars of $6.6M was more than the $6M generated in the previous TWO quarters COMBINED.

Better operational control, not just better pricing drove results.

Company saved over $500K in shipping costs in the quarter by sourcing three new carriers.

Company started consolidating T&L + Mamamancini’s shipments to single customers into one truck, instead of two.

Consolidated storage facilities from six to four.

Reduced overtime for savings of over $250K.

Plant utilization is only 50%, significant volume leverage potential to improve gross margins over time.

Already winning new customers and getting deeper penetration into existing customers.

In Q3, “launched into three new customers and drove double-digit new items into existing customers, half of which were through our cross-selling of our new T&L products into legacy relationships.”

In Q4,”looking ahead to the fourth quarter, we have already successfully sold in and received orders from three new customers and shipped an incremental double-digit portfolio of new items into existing customers, further expanding the breadth and depth of our coverage.”

Macro tailwinds in place (investments always sound better with “macro” theme attached).

“This approach fits well with the significant pandemic-related lifestyle changes that consumers faced in the last three years, with many focusing more than ever on quick, clean, and fresh meals made with better ingredients at a price more affordable than eating out. On the other side of the counter, retailers continue to face significant supply chain and labor challenges and are seeking labor-efficient, reliable solutions for their hot bar, deli, and grab-and-go offerings.”

50% of company sales are private label.

Categories the company participates in are growing 8-12% a year.

Conference Call Comments We Found Interesting

The realization of our goal to shape MamaMancini’s into a one-stop-shop for these deli prepared food solutions has required a step change in our corporate structure in many ways. (NOTE: For those investors looking for “catalysts”, there you go!!).

On the cost front, we have designed and implemented new approaches to cost management, driving noticeable improvements in procurement, manufacturing, and logistics management capabilities. As Matt will mention later, our efforts to more efficiently manage labor costs, particularly overtime, outbound logistics, and cold storage are realizing noticeable returns, allowing us to reinvest in our business.

We put new financial and operational controls in place to help our teams and provide agility for sales and operations staff. The weekly and monthly cadence of meetings as well as the clear and actionable KPIs we put in place are allowing our teams to communicate easier, make decisions faster with more information.

We have already started to build out the finance function. For example, our new Controller started today, as well as filling critical needs in logistics and soon procurement.

Another C that Adam did not mention but is critical to the success inside the operation is consolidation. We’ve been addressing the need to take advantage of synergies across our business units, helping to gain efficiencies spanning every aspect of the supply chain. In Fiscal Q3, we created a dedicated shipping team to focus on consolidating both inbound and outbound freight across our New Jersey and New York facilities. This team was successful in sourcing three new carrier options, creating competition that was able to reduce overall freight costs by 200 basis points in Fiscal Q3.

Another consolidation focus during the quarter was on our third party storage. As MamaMancini’s Holdings is first and foremost a manufacturer and marketer of deli solutions, we recognize that we currently leverage the expertise of others when it comes to cold storage. We have utilized multiple locations to hold raw materials and pre-shipped finished goods in an effort to maximize our production capabilities in our plants. However, the saying too many chefs in the kitchen is fitting when recognizing that spreading products across multiple sites can be counterproductive. Fiscal Q3 began the process of consolidating these third parties down from six to four strategic locations, eliminating additional storage costs that were not creating value.

We continue to research our cold storage options, including, but not limited to, investing in a centralized facility between the business units that we would control. Our dedicated costing models have empowered the sales team to make smarter decisions with regards to pricing products to our retailers that not only reflect fair perceived value to shoppers but also provide margin to invest back to help promote our products and keep us top of mind. (NOTE: THIS IS VERY IMPORTANT FOR SUPPORTING HIGHER GROSS MARGINS)

Finally, in Q3, I took our Management team to PACK EXPO International in Chicago where we walked the show in a continued effort to find better technology to further increase the plant’s efficiencies. We came away with multiple opportunities and started putting ROI documents together that will be addressed with the Board over the next coming weeks. (NOTE: COMPANY HAS ALREADY INSTALLED A NEW MACHINE THAT COOKS PRODUCTS

So it’s really easy for a customer that—I’m going to make it up, say they already have our meatballs or our sausage and peppers, they know we have quality. They know we have service. It’s, "Hey, by the way, do you have some chicken or do you have some grilled vegetables or do you have some paninis?" We now have all of those. We didn’t have them before. So that’s how we’re getting in. The customers see the quality, see the service and quite honestly, it’s easier for them. If they make one phone call to fill the entire deli case, that’s much easier than having to call 25 people to do that. That’s the vision.

What is the longer-term potential for earnings and valuation?

It's tough to make predictions, especially about the future.

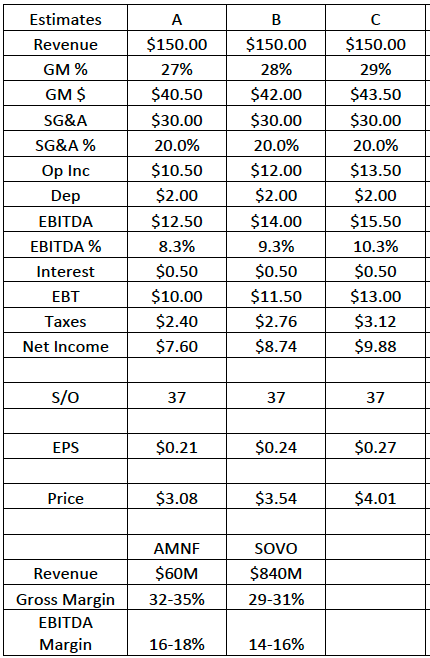

We have said in earlier posts that we only use models to get a general idea of how the business model works and generate a range of potential outcomes. So with that in mind, let’s take a stab at what the income statement could look like at $150M in revenue. This will drive the obligatory “what does this mean for the stock price” guesstimate!!!

Business model pre-mortem

Management believes there is significant opportunity to increase SKUs per EXISTING customer.

Our vision is to become a one-stop-shop for prepared foods for grocery, mass, club and convenience channels, addressing the $30 billion-plus food service and prepared foods market with our grocer partners.

Benefit to customer is reduction in the number of vendor relationships it has to manage and more likely to get volume discounts.

Company average is about 5.5 SKUs per 8000 doors. Note: Publix has 10 SKUs per store.

T&L increases the number of SKUs (i.e. chicken, paninis, olives) that can be cross sold to existing customers. Early results are positive, but sustainable?

If successful, this strategy could increase sales 20-30%.

No one has been successful at dominating the deli opportunity, so this is a new industry strategy that could fail due to apathy or inertia of customers.

Management believes there is significant opportunity to increase regional penetration in current customers.

It is our understanding that the company does not sell into 100% of all the available stores with current customers.

If successful, this strategy could increase sales 10-20%. (Just a guess).

There are reasons why this hasn’t happened before. Is current sales force/broker network up to the task? Does something have to change at customers (new buyers or management)?

Using product innovation to open new markets.

Meatball in a Cup ($1.25-$1.50 gross profit dollars per sale) example of this strategy.

Opens up convenience stores hot bars and food service opportunities which doubles market size.

Company has mentioned tangent product lines that can be developed internally to increase customer penetration (Pizza, Soup).

Meals for One. Reduces labor costs for grocery store operators.

These are in the very early stages of rollout. Even though these products make intuitive sense to us (Meatball in a Cup has a strong low $ cost per protein and Meals for One are on trend and labor saving for customer), Widespread adoption is not guaranteed. It would take a LOT of Meatballs in a Cup sales to move the needle (Selling 1 million a year would be 2800 a day and still generate only about $1.5-$1.9M in gross profits to company).

Kroger is still huge opportunity.

Company has not been able to penetrate into the largest grocery change in the country.

Company has relationship with Albertsons, so if Kroger is successful with their acquisition, that might EVENTUALLY provide the opportunity to sell to Kroger. We think the sales cycle could be as long as 2-3 years because of integration focus initially.

Haven’t heard specific reasons from management about why they have failed here. Several salesmen have tried and been replaced.

Operating Assumptions

Sales $150M.

GM 27-29%. (Note: peers have gross margins of 31-35%)

Depreciation and Amortization stays at $2M.

EBITDA Margin 8-10%.

While the comps we used have EBITDA margins about half of Gross Margins, we should note that T&L division that was acquired had 10-12% gross margins as is now at least 20% of sales, which limits upside of margin expansion.

All growth is organic. No increase in leverage.

PE is 15X

NOTE: Armanino Foods of Distinction (AMNF) sells frozen pasta and pesto sauces primarily in three states (CA, NV, AZ). Sonos Foods (SOVO) sells pasta sauces, dry pasta, soups, frozen entrees, yogurts, pancake and waffle mixes, other baking mixes, and frozen waffles under the Rao’s, Michael Angelo’s, noosa, and Birch Benders brands.

EV/EBITDA Assumptions

Company generates ZERO FCF. (Very conservative in our opinion, but keeps it simple).

Net Debt stays at $8M for EV calculation.

We are assuming 100% organic growth.

No new debt for acquisitions.

No debt paydown or cash accumulating on balance sheet.

This seems very conservative and may overstate our EV calculation (meaning or EV adjusted price per share may be too low.)

Assumes no real increase in shares outstanding. Shares probably do increase somewhat, offsetting some of the error in the no FCF assumption.

No time table for achievement of sales and margin goals.

Summary:

From 2016 through the first half of 2022, the company great revenue from $18M to over $60M, but gross margins collapsed from 40% to 16%. There was clearly a lack of control over major costs and pricing. In less than 120 days, due to attention to detail and a professional approach to running a business, new management was able to recapture over 1200bps of gross margin. We think the company is in the early stages of returning the company to a sustainable 8-10% EBITDA Margin business, while at the same time maintaining its long-term growth potential. We do expect the company to reinvest some of the savings to drive revenue growth and do not expect a return to the 30%+ gross margins of the past, or even the two peers we used.

However, we are confident that the company will be run more cost-efficiently than it has been in the past, which should eventually lead to a higher valuation. The company is currently trading at an EV/sales of about 75%. CPG companies typically trade for 1-3X EV/Sales. Even after the 80% jump in the stock, investors are skeptical of the future margin potential and EPS growth rate. If the company can achieve $150M in sales, 1X EV/Sales would be about $4 per share in stock price alone. One quarter does not make a trend, but we believe the company has a greater chance for success under this management than at any point in the last six years. (No offense Carl, we still love you!!).

Disclaimer

Investing501 uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The articles and reports published by Investing501 constitute the author’s personal views only and are for entertainment purposes only. They are not to be construed as financial advice in any shape or form. Investing501 does not predict the price at which the securities of any company may trade at any time. Every investor has different strategies, risk tolerances and time frames. You are advised to perform your own independent checks, research, or study, and you should contact a licensed professional before making any investment decisions. From time to time, the author may hold positions in the stocks mentioned in articles published by Investing501. To the extent the author does have such positions, there is no guarantee that he will maintain such positions. Neither the author nor any of its affiliates accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.

Adam L. Michaels, Chief Executive Officer of MamaMancini’s, will host a virtual investor presentation followed by a question & answer session. To participate, please click on the webcast link below:

Diamond Equity Research Emerging Growth Invitational

Date: Wednesday, January 25th, 2023

Presentation Time: 9:40 a.m. Eastern time

Webcast: https://us02web.zoom.us/webinar/register/WN_UmZJMSZ4TJ-O9Nn_M1fGVw