EARLY THIRD QUARTER REPORTS – SOME RELIABLE DATA POINTS – AND A (perhaps) SURPRISING CONCLUSION

Guest Analysis from Roger Lipton at Lipton Financial Services.

We work with Roger on various projects and restaurants are one our of favorite industries to analyze. We compiled a significant amount of data from the latest conference calls for Roger and we wanted to share his conclusions. Here is a complimentary post from his newsletter, which you can subscribe to here.

EARLY THIRD QUARTER REPORTS – SOME RELIABLE DATA POINTS – AND A (perhaps) SURPRISING CONCLUSION

Reporting season, representing the quarter ending September’22, is upon us. The seventeen companies we report on below all have a large number of company-operated locations, therefore providing us with a good indication of industry wide trends. We look first at the prime costs, Cost of Goods and Store Level Labor, then provide the Store Level EBITDA margins from ’21 to ’22. We follow the EBITDA trends by highlighting Q3 traffic trends. After our Q3 summary, we can’t help but philosophize a bit.

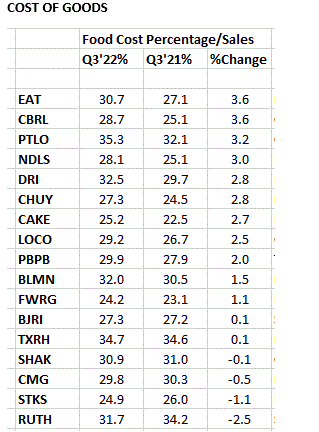

COST OF GOODS AND MARGIN TRENDS

Cost of Goods, shown in the table just below, ranked from highest to lowest YTY penalty, shows how shortages and higher prices of many commodities penalized Brinker (EAT) and Cracker Barrel (CBRL), by a fairly dramatic 360 basis points. Less affected were First Watch (FWRG), BJ’s (BJRI) and TX Roadhouse (TXRH) with relatively flat comparisons. Steak purveyors like One Group Hospitality (STKS) and Ruth’s Chris (RUTH) benefited from lower beef prices. Generally speaking, most of the public companies have increased menu prices below the inflation rate. That is the major reason for the large contraction of gross margin at the companies showing the worst relative performance.

STORE LEVEL LABOR

Store level labor generally did not hurt the YTY comparisons very much. Wage inflation was prevalent, up from 6-10%, but productivity was improved in many cases as post-Covid staffing became more normalized. Higher menu prices also helped, of course. The worst results, at El Pollo Loco (LOCO), Chuy’s (CHUY) and Cracker Barrel (CBRL) were all a result of understaffing a year earlier. We have adjusted LOCO’s numbers below to eliminate the Employee Retention Credit (ERC) they received last year.

STORE LEVEL EBITDA MARGINS – AND TRAFFIC TRENDS

The table just below shows the resultant store level EBITDA margins, shown from worst to best. Also a factor within the store level bottom line are “Other Operating Expenses” (not shown) such as Utilities, Occupancy, Insurance, etc. Safe to say that none of these categories have declined in absolute values, and often have increased as a percentage of sales as well. The numbers below are self-explanatory, as store level EBITDA got squeezed from a high of 580 bp at Brinker (EAT) to relatively flat results at BJ’s (BJRI), Ruth’s Chris (Ruth), and TX Roadhouse (TXRH). The best store level EBITDA comparisons were at Shake Shack (SHAK), which benefited from a recovery in their city-based stores, Chipotle (CMG), which continues to have great success with their digital ordering capability, and Potbelly (PBPB), which is improving operations on a broad front.

In conjunction with the store level EBITDA margin comparisons, we provide a brief summary of traffic/sales trends. Lastly is our conclusion relative to Q3, and a long term overview.

CONCLUSION:

Dining away from home is increasingly becoming a lifestyle choice, rather than a necessity. Traffic/location is generally down and Flat can be considered the new Up. Menu prices have been adjusted, by high single digits in the last twelve months, and the high teens since 2019, but superior operators must maintain, and hopefully build, traffic trends. The decline in store level margins has become obvious, and will not be easily reversed. The rate of wage inflation is expected to moderate and commodity prices (in such items as beef, chicken wings or cheese) may provide some short-term relief, but utilities and other store level expenses continue their ascent. Lower store level margins combine with a materially higher cost of construction to provide materially less attractive cash on cash returns. Of further concern: much higher interest rates and the correspondingly lower equity valuations have provided a much higher cost of capital, so operators must more cautiously approach both new locations and renovation of existing units.

Our long term overview:

We are not pessimistic regarding the outlook for the restaurant industry. The higher level of competition, the necessity to provide a differentiated product to an increasingly discerning public, the adjustments coming out of almost three years of pandemic driven distortions, are not unique to the restaurant industry. As opposed to many other industries, however, consuming food as fuel is not a choice. It’s just a question of who will provide the necessary price/value. One of the great aspects of the restaurant industry is that success requires only a reasonable degree of intelligence and a strong work ethic, certainly not an MBA or PHD. As difficult as it has become for some mature chains to maintain their mojo and their margins, there are always operators who are writing a new chapter. That’s where operators should position their careers, and investors should place their bets.

Roger Lipton