Can BT Brands Unlock Value at Noble Roman’s?

In November of 2022, BT Brands (BTBD) filed a 13D after accumulating a 4.38% stake in Noble Roman’s (NROM). On February 16th of 2023, the company amended its 13D after increasing its stake to 5.68%. In this post, we will discuss what BT Brand is proposing and analyze the potential to unlock value for NROM shareholders. This post looks at the proposal and the operations of the franchise business and not the Craft Pizza business. NROM is scheduled to report earnings soon and a follow up post will be forthcoming to analyze any management response to the proposal and the entire business.

Overview:

· On November 28th BTBD filed a 13D on NROM after accumulating a 4.38% stake in the company Check.

· On February 16th BTBD filed an amended 13D showing it had increased its stake to 5.68%.

· Corbel Financing agreement in 2020 includes high interest rate and potential shareholder dilution.

o In February of 2020, NROM entered into a Senior Secured Promissory note and Warrant Purchase Agreement with Corbel Capital Partners to boost the company’s liquidity position during Covid. The Agreement included a very high interest rate, a PIK feature which compounds the interest expense and potentially highly dilutive warrants (9.2% of company).

o Terms of the Agreement

§ $8M Senior Secured Promissory Note.

§ Cash interest rate of LIBOR + 7.75%.

§ PIK of 3% per annum, which is added to the principal amount.

§ Maturity February 7th, 2025.

§ Monthly payments of $33,333 beginning February 2023.

§ Warrant to purchase up to 2.25M shares of stock. Expires 2026.

· 1.2M exercisable at $0.57 per share

o Forced exercise if stock is trading above $1.40

· 900K exercisable at $0.72 per share

o Forced exercise if stock is trading above $1.50

· 150K exercisable at $0.97 per share

o Cashless exercise.

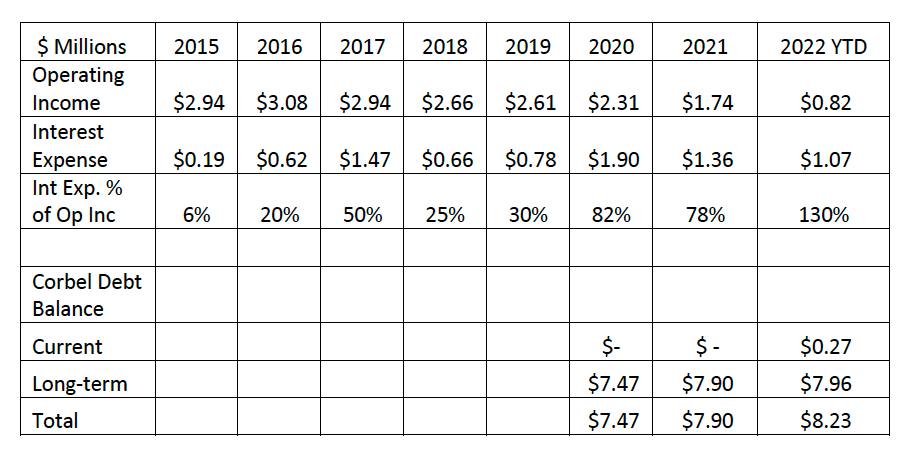

The problem the company faces is that the PIK feature of the note is steadily increasing the interest expense as a percentage of operating income. Interest expense currently exceeds operating income and will continue to grow unless alternative financing is used. This issue needs to be addressed by management immediately. The BT Brand offer significantly improves the company’s finances in a non-dilutive way, which is a very positive outcome for shareholders.

Rising Interest Costs are a Problem.

Interest expense is consuming over 130% of operating income. This is an unsustainable situation that needs to be address immediately. This makes the BT Brands proposal intriguing for shareholders.

The BT Brands Proposal:

In our opinion, the BT Brands proposal is a very attractive solution to reduce the significant interest expense burden on the company. As a current shareholder we are pleased to see such a simple and non-dilutive solution to the current onerous financing situation. The main points of the proposal are as follows:

· A $2M loan at a 5% interest rate for two years.

o This is an extremely attractive interest rate in today’s operating environment and would certainly not be available to the company through any other lender, including Corbel.

o BT Brands has over $8M in cash, so conceivably it could lend even more money to NROM if necessary.

o Reducing net interest costs by $250K a year.

· NROM grants BT Brands to designate two new board members, bringing the total to seven.

o This proposal seems reasonable.

o It does not ask for control of the board.

o CEO and CFO have substantial restaurant industry experience.

Excerpts from 13D:

· As noted in the Original Filing, the Reporting Persons engaged in discussion with a member of the Board of Directors of the Issuer, including a discussion by the Reporting Persons (and certain of their affiliates) as to possible approaches to refinance on better terms the Issuer's approximate $8.5 million senior secured promissory note bearing a current interest at the rate estimated to be approximately 17% per annum. Beginning in February 2023, the Company’s senior debt, “Corbel Note,” requires Issuer to make minimum monthly payments of approximately $33,333, in addition to current interest. Over the next 24 months, the aggregate monthly required payments exceed the Company's on-hand cash. Issuer cash was reflected in its most recent SEC Filings as $742,989 before a required February note payment of $125,000; if made, this payment further reduced the cash balance. Given the recent increase in the floating LIBOR, the 3% payment-in-kind (“PIK”) interest accruing under the Corbel Note may result in a minimal reduction or a possible negative amortization of the Corbel Note loan balance. Based on the current LIBOR, the required loan payments will rapidly consume the Company's available cash balance.

· Since the original filing date, BTB has sent correspondence to each member of the Board of Directors and the entire Board of the Issuer. Among other things, correspondence to the Board noted the financial expertise of the independent directors and their ability to evaluate the financial and liquidity issues of the Company, including the proposals of BTB. In its most recent correspondence to the Issuer on February 13, 2023, BTB offered to lend the Issuer $2 million for two years at a fixed rate of 5%, with the amount advanced being used to pay down the balance on Corbel Note. The Corbel Note carries a variable interest currently estimated at approximately 17% per year. A $2 million paydown of the existing senior debt would reduce net annual interest costs by approximately $250,000. BTB believes reducing interest expense will contribute to the Issuer achieving profitability. BTB offered to work with the Issuer introducing the Issuer to investment bankers to facilitate senior debt refinancing. BTB noted that refinancing the current debt, depending on the final terms, could reduce the annual interest cost by more than $800,000. In consideration of its loan to the Issuer, BTB proposed that the Issuer grant BTB the right to designate two new representatives as additional members to the Issuer's Board of directors. The Issuer, through its chief financial officer, declined BTB's offer without entering into discussions with BTB regarding its proposals.

· Such communications and discussions may also relate to one or more potential extraordinary corporate transactions involving the Issuer, including a possible change of control, business combination or other strategic transaction involving the Issuer (such as a merger, tender offer, reorganization, sale of a material amount of assets or similar transaction), potential changes to the composition of the Board or management of the Issuer, as well as potential changes to the strategic direction, capitalization or governance of the Issuer. The Reporting Persons (or their affiliates) may submit to the Issuer proposals relating to such matters and may take other steps seeking to bring about changes to increase shareholder value of the Issuer. There can be no assurances that any such proposals will be submitted or that any transaction will result from any such discussions or proposals. The Reporting Persons (or their affiliates) are under no obligation to propose or consummate any transaction.

Who is BT Brands?

BT Brands came public 2021 and owns thirteen restaurants. The company has a history of acquiring ownership in restaurant concepts. The company could bring its expertise to helping NROM grow its Craft Pizza division.

Business

As of October 2, 2022, BT Brands owned and operated thirteen restaurants, including nine Burger Time restaurants in the North Central region of the United States, a Dairy Queen fast-food franchised location in suburban Minneapolis, Minnesota, collectively ("BTND"). Following the end of the third quarter on November 6, 2022, the Burger Time in West St. Paul, Minnesota was permanently closed. The Company is considering alternate uses for the site. We own Keegan's Seafood Grille ("Keegan's"), a dine-in restaurant located in Florida, Pie In The Sky Coffee and Bakery ("PIE"), a casual dining coffee shop bakery located in Woods Hole, Massachusetts, and the Village Bier Garten, a German-themed restaurant in Cocoa, Florida.

On June 2, 2022, BT Brands purchased 11,095,085 common shares representing 41.2% of Bagger Dave's Burger Tavern, Inc. ("Bagger Dave's"). We acquired the shares from its founder for $1,260,000, or approximately $0.114 per share. Following the investment, representatives of BT Brands were appointed to two of the three positions on Bagger Dave's Board of Directors.

BTBD Management:

The two main principals of BT Brands have extensive backgrounds in restaurant operations. The CFO spent thirteen years at Landry’s Restaurants and five years at Rainforest Café. We believe if these two executives joined the NROM board, they could add significant experience in both operations and finance.

Gary Copperud has served as the Chief Executive Officer and a director of the Company since July 31, 2018. He was a founding member of BTND, the previous owner of Burger Time, in 2007 and served as BTND’s managing manager and Chief Financial Officer from its inception until July 31, 2018. Mr. Copperud has been a managing director of BTND Trading, LLC, an entity unrelated to BT Brands, since 2016. Mr. Copperud was a founding stockholder of Next Gen Ice, Inc., a provider of automated ice delivery systems,, in June 2019, and has served as the Chairman of the Board of Next Gen Ice since July 2019. We believe Mr. Copperud’s long tenure as a managing member of BTND, as well as his prior experience as a member of the board of directors of a public company, qualifies him to serve on our board of directors. Mr. Copperud is not an “independent director” as such term is defined by the Rules of The Nasdaq Stock Market.

Kenneth Brimmer has served as the Chief Operating Officer, Chief Financial Officer, Chairman of the company’s board of directors and Principal Accounting Officer since July 31, 2018. Mr. Brimmer also has served as a member of the board of directors of Next Gen Ice, Inc. since October 2019 and currently serves as the Chief Financial Officer of Next Gen Ice, Inc. Mr. Brimmer has a wide range of experience, including several early-stage and rapidly growing businesses, serving at various times as President, Chief Executive Officer, and a director and Audit Committee Chairman of several public and private companies. Mr. Brimmer previously was the Chief Executive Officer of Hypertension Diagnostic, Inc. and was its CEO from September 2012 until May 2020. Mr. Brimmer is the CEO of privately held Brimmer Company, LLC, which has provided consulting management services to BT Brands and Next Gen Ice, Inc. Mr. Brimmer was a Director of Landry’s Restaurants from June 2004 until April 2017 and served on the Audit and Compliance Committee of its Golden Nugget – New Jersey Casino. Previously, he was President of Rainforest Cafe, Inc., which grew from start-up to over 6,000 employees from April 1997 until April 2000, and he was Treasurer from its inception in 1995 until April 2000. During the time Mr. Brimmer served as Treasurer of Rainforest Cafe, Rainforest raised over $200 million in a combination of private and public stock offerings. Prior to Rainforest, Mr. Brimmer was employed by Berman Consulting, LLC, a financial and investment management company, from 1990 until April 1997. Mr. Brimmer has a degree in accounting and worked as a certified public accountant (inactive) in the audit division of Arthur Andersen & Co. from 1977 through 1981. We believe Mr. Brimmer’s long and varied career as a business executive, particularly his service as the chief operating officer of a major restaurant chain, qualifies him to serve on and chair our board of directors. Mr. Brimmer is not an “independent director” as such term is defined by the Rules of The Nasdaq Stock Market.

We believe adding two new members to the board and utilizing the extremely attractive financing option would significantly improve the governance and financial health of the company and provide the opportunity for the company to grow both its Craft Pizza store base at its pizza franchise business.

There have been several things about NROM that have concerned us, and we suspect, other shareholders when it comes to governance and disclosure issues. We will discuss some of them in the next section.

Closer look at operating history and disclosures. More questions than answers:

· Write-offs of receivables

o From 2015-2020 the company wrote off nearly $9M in receivables due to lack of collectability. These were originally classified as long-term receivables due to their past due status.

o The company disclosed that “some receivables arose from the Company incurring legal fees to enforce the franchise agreements and other collection cost which adds to the receivables in accordance with the agreements.”

o There was no additional disclosure as to the amount of legal fees that were added to the receivable balance. In our opinion, a more conservative accounting approach would have been to expense these legal fees as incurred and quantify them publicly, especially if they were material.

Disclosures in Franchising Division Make External Analysis Difficult

Revenue Per Franchisee is Declining

o Trade Show and Travel Expenses Seem High

§ Trade show expenses have been extremely stable at 7% of revenue, except for 2020 and 2021 when a decline in revenue increased the expenses to 9% of revenue.

· With in-person trade shows virtually shut down for all of 2019 and 2020, it is difficult to understand how the company spent $420K a year on trade show expenses. In absolute terms, the amount also seems excessive relative to the attendance fees associated with typical trade shows.

· It is also interesting that the trade show expense as a percentage of revenue remains so stable. There is also no explanation as to why trade show expenses have declined in line with revenue. Are they attending fewer shows? Are they doing fewer things per show (exhibitor booths), are the fees per show declining?

§ From 2016 through Sept 2022, the company spent almost $4M in tradeshow fees and travel. Over that time the company has only increased its franchisee base by 10% (301 on a net basis). In addition, the average revenue per franchisee has declined nearly 50% ($2,600 per franchisee to $1,240 per franchisee). Some of this may be the result of a higher number of convenience stores (relative to grocery stores) in the system.

· However, the decline in revenue per store is even more disappointing considering what is happening in the pizza convenience store franchise industry.

o Conversations with Hunt Brothers, the largest operator in the space indicated that Covid was a huge boost to its business and that the company is setting “sales records every week.”

o The Hunt Brothers representative we talked to indicated that Covid changed the behavior of how people in rural locations utilized the convenience store pizza option. Customers began taking home whole pizzas more frequently, which significantly increased business. That volume has continued to increase.

o The representative we talked to also indicated that the addition of a freshly prepared hot food option in a convenience store increases sales (excluding fuel, lottery tickets and cigarettes) by about 30% because of the higher attachment rate of high margin drinks and other snacks. 7-11 is pushing pizza in their stores (including for delivery). The pizza in convenience stores is clearly a growing industry and NROM could be a leader in the space.

· To be clear, we are not saying that there is anything nefarious about these expenses, but we do feel more disclosure is necessary in order for shareholders to understand the profitability of the division.

o Other Expenses seem high for a franchisee fee-based business.

§ The composition of the $619K in other expenses is not disclosed.

§ The company says that it collects the franchise fees by ACH. It is difficult for us to understand why it takes over $1.3M in salaries, wages and other expenses to collect these fees. Without more disclosure from management, it is difficult to understand why these expenses are being incurred.

o The company also does not seem to know how many of its franchisees are actually paying them. This is extremely concerning and shows a lack of management control of this part of the business.

§ This disclosure is in every 10K:

· Grocery stores are accustomed to adding products for a period of time, removing them for a period of time and possibly re-offering them. Therefore, it is unknown how many grocery store licenses, out of the total count of 2,403 have left the system.

· The company claims that because its fees are collected through distributors, it does not have the ability to know which specific franchisee is paying.

· In 2019, there was also a large increase in the number of grocery stores in the system that was not accounted for in the reported language. The company showed an increase of 300 grocery stores, but stated that there was no net increase in new franchisees in total.

o Executive compensation seems excessive relative to market capitalization.

The CEO and CFO make a combined $750K in compensation. In 2020, they actually agreed to reduce their compensation from a combined $1.2M. While this action is certainly a move in the right direction, the $750K in combined compensation is still substantial in relationship to the $7M in market capitalization of the company. The CEO and CFO are clearly extracting significantly more value from the company that the company is leaving for shareholders.

o Employment Agreements

§ Paul W. Mobley has an employment agreement with the Company which: (A) fixes his base compensation at $650,000 per year for 2021 (although Mr. Mobley voluntarily reduced his base compensation to $300,000 for 2020 and 2021 and pursuant to an agreement entered into in conjunction with the Corbel financing in 2020 Mr. Mobley agreed to limit his salary in future years to a 5% per annum increase); (B) provides for reimbursement of travel and other expenses incurred in connection with his employment, including the furnishing of an automobile and health and accident insurance similar to that provided other employees; and (C) provides life insurance in an amount related to his base salary. The initial term of the agreement is seven years and the term automatically renews each year for a seven-year period unless the board of directors takes specific action to not renew. The agreement is terminable by the Company for cause as defined in the agreement. The agreement does not provide for any benefits payable as a result of a change of control of the Company.

§ A. Scott Mobley has an employment agreement with the Company which: (A) fixes his base compensation at $551,000 per year for 2021 (although Mr. Mobley voluntarily reduced his base compensation to $444,568 for 2020 and 2021 and pursuant to an agreement entered into in conjunction with the Corbel financing in 2020 Mr. Mobley agreed to limit his salary in future years to a 5% per annum increase); (B) provides for reimbursement of travel and other expenses incurred in connection with his employment, including the furnishing of an automobile and health and accident insurance similar to that provided other employees; and (C) provides life insurance in an amount related to his base salary. The initial term of the agreement is five years and the term automatically renews each year for a five-year period unless the board of directors takes specific action to not renew. The agreement is terminable by the Company for cause as defined in the agreement. The agreement does not provide for any benefits payable as a result of a change of control of the Company.

o Unexplained extension of over 1.3M in options that were set to expire in 2021 and the granting of 330K additional options is concerning.

§ The company did not file a proxy in 2020. However, when comparing the options table in the 2021 proxy statement to the 2019 proxy statement, there were 1.335M options that were set to expire in 2020 and 2021 that had their expiration dates to 2023. The CEO and CFO were also granted an additional 330K options with strike prices of $0.40 and $0.60 and expiration dates in 2029 and 2030. As shareholders we are extremely disappointed that the board would extend the maturity dates on options that are significantly dilutive to existing shareholders.

Putting It All Together

Due to the impact of Covid on its business, NROM secured $8M in financing for Corbel that included an interest rate that was LIBOR +7.75%, a 3% PIK and warrants that would give Corbel up to 9.2% of the company if exercised. At the time, management believed this was the best option for the company to continue to survive and continue to operate. However, since agreeing to the terms, interest expense as a percentage of operating income has increased to over 130% and the all-in costs of the financing are approaching 15-17%. The potential 9% dilution to shareholders is also looming.

BT Brands has made a proposal to the company that helps address this problem in a very attractive way to current shareholders. The interest rate of 5% is significantly better than the terms of the Corbel financing and also significantly better than terms the company would receive from any other financing source. There is NO DILUTION to current shareholders, which again, is almost unheard of in the current operating environment for financing of micro-cap companies. The proposed addition of two new board members is also highly appealing to current shareholders. It does not give BTBD control of the board but brings fresh eyes and experience that can help the company improve its operations, governance, and disclosure issues. The fact that the CFO has refused to engage in serious discussions with BTBD or publicly disclose any other financing options that are equal or better to the BTBD proposal is EXTREMELY DISAPPOINTING. The fact that the board (including the CEO and CFO) have not engaged in serious discussions could also raise serious breach of fiduciary responsibility issues.

Could BTBD start a proxy contest or takeover if management continues to stonewall them and could it be successful?

Just glancing at the ownership table in the latest proxy would seem to indicate that BTBD would have an uphill batter to win a proxy contest. However, the proxy table overstates the ownership of Corbel and management because it includes all options (almost all of which are not exercisable at the current price.). Adjusting for actual shares held by management and the fact Corbel owns no shares directly, ownership of the CEO and CFO drops to approximately 13%. We believe that the Stiller estate has sold all of its holdings since the proxy statement was released. This means BTBD is now most likely the second largest shareholder of NROM stock. This increases the potential for success of a proxy contest or takeover by BTBD. An outright acquisition could be highly accretive to BTBD. The company could reduce expenses significantly (CFO/CFO/COO salaries of over $800K, reduction of $800K in interest expense, potential to eliminate $1-2M in overhead expenses in NROM two divisions). Between the CEO/CFO and Corbel they are extracting almost $2M in cash out of a company with an equity value of $7M. Even with a significant premium and the inclusion of some of the warrants and options, there could be significant value for BTBD and its shareholders to just acquire the company instead of offering financing and board members.

It appears as though BTBD has offered NROM an offer it can’t refuse to help improve its current financial situation. The lack of a response by NROM management and board is both disappointing and surprising. The board has a fiduciary responsibility to consider all offers to help the company and improve the outcome for shareholders. We look forward to the 2022 year-end financials and conference call. Hopefully NROM management will address the financing problem and explain its reluctance to engage with BTBD in meaningful discussions.

Ownership Adjusted For Non-in-the-money Options

Disclaimer

Investing501 uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The articles and reports published by Investing501 constitute the author’s personal views only and are for entertainment purposes only. They are not to be construed as financial advice in any shape or form. Investing501 does not predict the price at which the securities of any company may trade at any time. Every investor has different strategies, risk tolerances and time frames. You are advised to perform your own independent checks, research, or study, and you should contact a licensed professional before making any investment decisions. From time to time, the author may hold positions in the stocks mentioned in articles published by Investing501. To the extent the author does have such positions, there is no guarantee that he will maintain such positions. Neither the author nor any of its affiliates accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.